Affordable housing finance is an idea whose time has come

-

Loading...

Loading... - Dhruv Patel

- 13 Jun 2022

- 252 Views

- 0 Like

- 0 Comment

What will it take to increase affordable housing finance in Bangladesh?

Consider this: the path to affordable housing for lower income groups requires that financial institutions negotiate the triple obstacles of informal property and informal income, a lack of long-term finance, and weak titling and foreclosure laws.

For most financiers, that is a triad of trepidation – few lenders would venture into such a space.

Yet the housing market, if it could safely be tapped, offers tremendous benefits. And it is a market whose time has come. A combination of political will and capacity building could change the game for the better.

The demand

Existing demand for urban affordable housing is approximately 6mn units, and is expected to rise to 10.5mn units by 2030, says Nuzhat Anwar, the acting country manager for the International Finance Corporation in Bangladesh.

Roughly 67 million people live in urban areas as of 2020, according to Anwar. By 2030, she estimates that half the country’s population could be city dwellers.

The IFC estimates that the current financing gap is approximately $59 billion for some 3.5 million residential units.

To meet this demand, home loans worth $2.5 billion have to be disbursed annually. Yet mortgage penetration in Bangladesh is just 3%, Anwar says.

For comparison, it should be noted that mortgage penetration in India is 10%. In the developed world it is between 50-70%.

Housing, she explains, has not been a priority sector. There is no technical definition of affordable housing, and no separate regulatory framework for banks and NBFIs regarding housing. The market has also been held back by difficulties in titling and a lack of foreclosure laws.

But affordable housing financing is possible as long as “the legal framework and enforceability” and “the regulatory framework of completing the process” supports it, according to Naser Ezaz Bijoy, country CEO, Standard Chartered Bank Bangladesh.

Ten percent of bank and NBFI financing goes to housing, but the capital markets have not been tapped.

Life insurance funds, pension funds and sovereign funds could play a bigger role, but there needs to be confidence in the ability to repossess assets if needed, Ezaz says.

Since the urbanization ratio correlates directly with economic prosperity, if the country hits its target of achieving high-income status by 2041, then the urbanization ratio could reach 60%.

Ezaz calculates that if Bangladesh’s population hits 200mn people by 2041, that would mean that some 120 million people – nearly twice as many as now – would be living in urban areas. And they would need a place to live.

Housing currently contributes 8% directly to the economy, and construction 8.4% indirectly.

Ezaz explained that the repayment track record of the affluent market segment and first-time home owners was good.

The aspirant segment who leveraged their properties in more speculative investments, were not as credit worthy and banks have had a lower risk appetite for such borrowers.

Enabling supply

Two leading problems are the cost of financing and the need for long-term finance.

McKinsey has estimated that globally, affordable housing will cost $16 trillion in the ten years leading up to 2025, of which less than a fifth will likely come from the public sector.

That means that the bulk of financing will have to come from the private sector: from private investors and from the capital markets, so that long-term investors can enjoy the returns on long-term assets.

The public sector’s role, then, will have to be as an enabler: it must enable a safe and dependable regulatory framework in which long-term financing can flourish.

On the demand side, the major constraints are the high cost of mortgages and the lack of affordability for many.

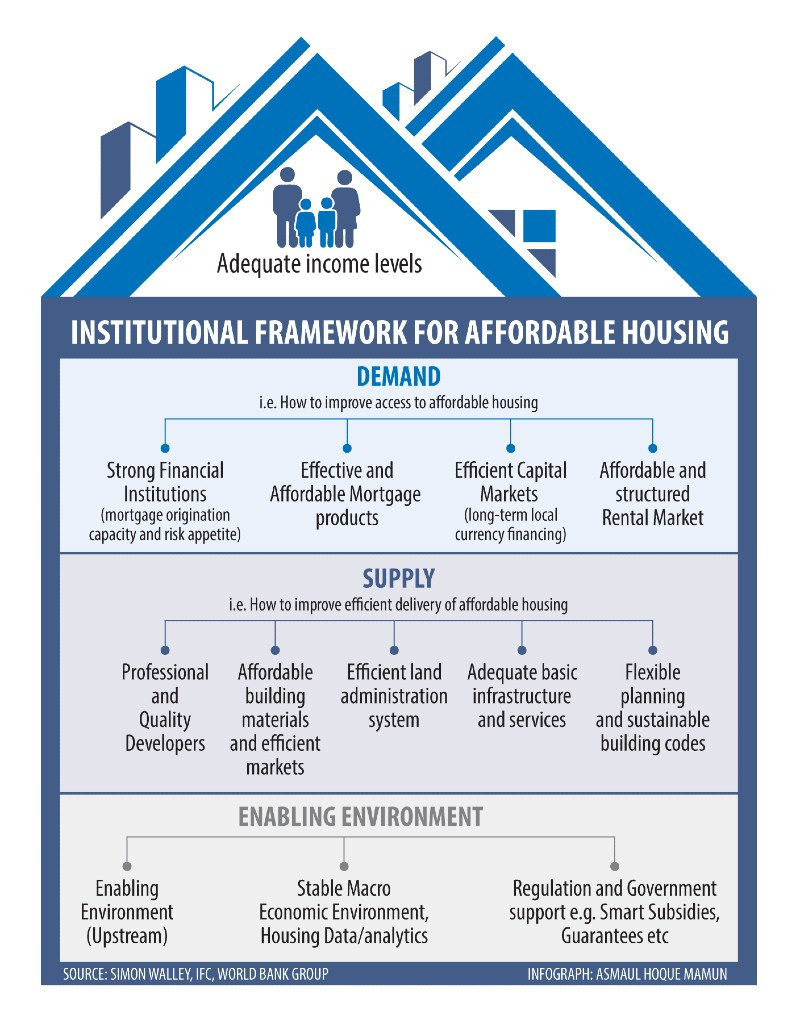

The reasons for this, according to the IFC’s Simon Walley, lead specialist at the Finance Competitiveness and Innovation Global Practice, include informal incomes, difficult property titling regimes, a lengthy foreclosure process, regulatory regime with caps, lack of long-term finance for mortgage lenders, and the limited capacity of financial institutions to expand in the housing finance business.

Fixing these concerns will make it easier to securitize asset-backed loans and set up REITs to leverage the capital markets. REITs provide access to a large pool of investors to benefit from income generated by properties without their owning the properties. Read More...